It’s easy to be unsettled when the same names seem to dominate every performance table. The U.S. weight in global indices is high at ~65%, technology looms large at ~30%, and the biggest companies feel all‑important – the top ten largest stocks now account for around ~25% of the global market. It can feel like the same story on repeat.

Recent decades remind us that market leadership changes over time. These episodes have come and gone across sectors, styles and countries – energy and autos in the early 1980s, Japan in the 90s, ‘Dot com’ stocks at the turn of the millennium, and so on. Today’s concentration is notable, but not unprecedented.

Figure 1: It’s hard to stay at the top forever

That won’t stop the headlines. Narratives about ‘overpriced tech’, ‘bloated U.S. markets’ and ‘inevitable decline’ are everywhere. The diagnosis is often similar, the prescriptions, wildly different. Should you underweight the U.S. or tech? Bias towards home markets? Add gold, private equity – or even Bitcoin? Or is it time to head for cash? The lack of consensus is telling: these views are already reflected in today’s market prices, just as those betting that U.S. tech will keep leading the charge are too.

Part of constructing an evidence-based portfolio means accepting that markets work well and are thus extremely difficult to second guess consistently. That does not mean that your portfolio is not suitably diversified if one or more of the above narratives come to pass. Rather than relying on what any speculator might suggest, your portfolio uses markets to deliberately ‘tilt’ towards stocks whose smaller size and relatively low prices suggest they exhibit higher risks than those large companies that dominate the market.

The benefits of this approach are twofold: firstly, if markets work, then the flipside of higher risk is higher returns, which ought to be enjoyed over time. Secondly, these riskier stocks tend to behave differently to the market, meaning a diversification benefit is on offer which should mitigate worst case scenarios – if one part of the portfolio is zigging the other might be zagging.

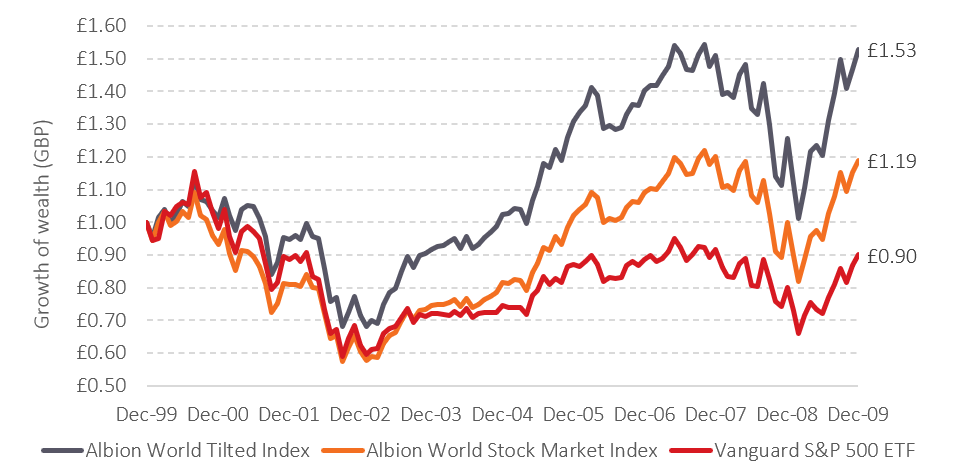

The chart below is a reminder of a scenario when this diversification had a real benefit to small and value tilted portfolios. At the turn of the millennium, ‘Dot com’ stocks were booming, the US was about 55% of the world market, the technology sector about 30% and valuations and stock concentrations were high. This is not to say history is to repeat itself, it almost certainly will not. However, it shows that parts of your portfolio will show up for you at different times. This is by design.

Figure 2: Tilted portfolios can mitigate worst case scenarios

Source: https://smartersuccess.net/indices. Vanguard (VOO). Returns in GBP.

Investing is not known for dishing out free lunches. One must accept that a small and value-titled portfolio can underperform for long periods, despite that not being the expectation. This is the price you pay for entry, and you must be able to stick with it through time to enjoy the long-term benefits on offer. The table below brings more context to the relative differences between a tilted portfolio and the market in the last century.

Table 1: Relative outcomes for a tilted portfolio versus world stock markets