This guest blog was written by Chris Budd, who wrote the original Financial Wellbeing Book as well as The Four Cornerstones of Financial Wellbeing. He founded the Institute for Financial Wellbeing and has written more than 130 episodes of the Financial Wellbeing Podcast.

A comment that one often hears when discussing finances is that people are “bad with money”.

What do they actually mean by this? And how can we change this, so that they are good with money (or at least, not bad!)?

Money Habits

Firstly, let’s consider what this phrase actually means.

Perhaps somebody is not very good at saving. Perhaps they feel they spend too much. Maybe they spend on things that, in hindsight, they feel they shouldn’t have spent money on.

It could be a more technical aspect, such as not being very good at investing. Perhaps they aren’t good at picking investments, or react emotionally, such as selling when markets have gone down.

What words might they use to describe being bad with money?

Framing

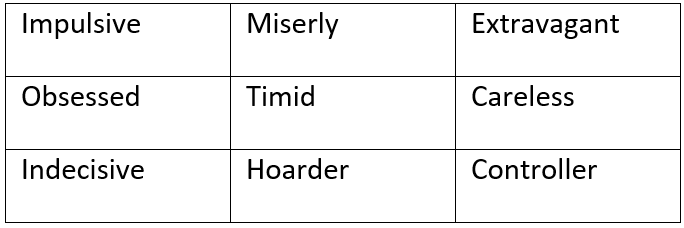

Try this exercise. Here are a bunch of negative attributes that can relate to money. Do any of these apply to you? Are there things that you want to change about yourself?

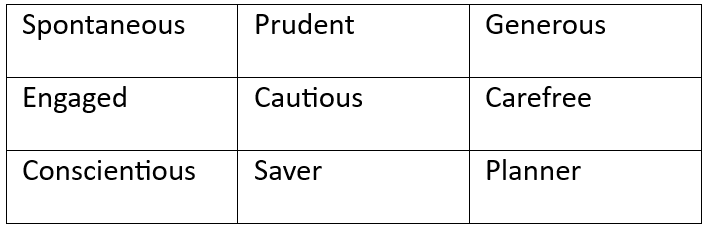

Next, here is a list of positive attributes that can relate to money. Maybe some of these apply to you. Perhaps there are things you rather like about yourself.

These words describe positively and negatively the same thing. Someone who could be criticised for being miserly might like the fact that they tend to be prudent. Someone who can be a bit of a control freak might also be extremely good at planning.

The chances are that at least a few of these attributes are ones we both don’t like and yet also do like about ourselves, depending on how they are expressed. Somebody who is impulsive may well make rash decisions, and yet they also like the fact that they can be spontaneous.

If you think you are not good with money, write down the behaviours that cause this. Next to those, write the positive version of that behaviour.

The next step is to consider whether these money behaviours are actually causing you a problem.

Problem or pleasure?

For example, an impulsive person may spend on things that they can’t afford. This could get them into debt or mean that they fail to achieve long-term objectives.

One solution to impulsive spending is to build a delay into your spending process. When you want to buy something, perhaps online, place it in the basket, but do not buy it. Put down the phone, and come back to that purchase in two days. If you still want it – and can afford it- then buy it. But you might now realise that you don’t really need it, in which case, remove it from your basket.

This is an example of how to improve your money behaviours, starting with recognising them. But we don’t always need to change our behaviours.

For example, someone might enjoy buying things that they don’t really need. If they can afford it and are on course to achieve longer-term financial plans, then there is not really a problem. Of course, it is very important to be sure!

The 2-step approach

Take a look again at that list of words that describe attributes that you don’t like about yourself. Are they causing a problem? If yes, then you could think about how to change these behaviours, such as the delayed spending tip to help with impulsive behaviour.

If it is not causing a problem, however, perhaps you could change the way you think about this behaviour by using the positive version of that attribute. Rather than thinking of the behaviour of yourself (or your partner) as being extravagant, for example, think of it as being generous.

Apply these two rules to all of your financial behaviours, and you will likely find that you are not only better with money, but you are also happier.

Please note:

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.